Consider l’affaire Sonics: The 2008 “move” (theft) of the Supersonics franchise from the city of Seattle to Oklahoma City.

(The basic story is covered in this wikipedia article as well as a recent deep dive in Luminary’s podcast Sonic Boom. I’m going to assume you’re roughly familiar with the outline: Starbucks billionaire CEO Howard Schultz buys the team in 2001. After a decade in which Seattle voters approved public funding for new football and baseball stadiums he decided to make a play for a publicly funded basketball arena. The bid failed for various reasons and he sold the team to an Oklahoma City group that was clearly going to move the team with David Stern’s approval. Later Schultz claimed he didn’t think they would actually move the team.)

What makes it interesting for our purposes is that the episode is so sordid and full of villains that most sober-minded people think David Stern is probably only the third or fourth worst person in all of it.

Are they right? So much seems to ride on the degrees of culpability in the big causal net that lead to this generational fiasco. Did David Stern make it happen or just let it happen? And if it was the latter can we even really blame him? Is this chapter really such a big deal considering everything else he got up to?

In order to answer that let’s go through the facts in a slightly different order and reframe exactly what was at stake for Stern, the Sonics and the NBA. We’ll go into detail about Seattle itself, and then correct a key misconception which has been allowed to enter the record unchallenged. Then we’ll re-examine some of the events and ask if the make-it-happen / let-it-happen dichotomy actually gets anyone off the hook, especially a certain Madison Avenue supervillain.

But first, our friends, from Pearl Jam:

Seattle’s suitability for an NBA team

Let’s imagine the perfect candidate city for NBA basketball. First of all, it should be rich. You want as much discretionary income as possible sloshing around to sell into. Check out these US government census links on Seattle and the Seattle area.

| Place | Population | Median Household Income |

|---|---|---|

| Seattle metro | 749,256 | $105,391 |

| King County | 2,266,789 | $106,326 |

| Seattle MSA | 4,018,762 | $101,721 |

| OKC MSA | 1,441,647 | $61,815 |

| Cincinnati MSA | 2,261,665 | $70,818 |

| borough of Brooklyn | 2,641,052 | $67,567 |

(sources: US Census quick facts, censusreporter.org,)

I’m only picking on Cincinnati and Brooklyn because they are also major league cities in two different parts of the country. You could roughly populate either one with only the half of Seattle households that are above the $100k+ median household income (MHI) mark. Within Seattle is a shimmering Golconda larger and much wealthier than Cincinnati, Brooklyn, Indianapolis (2.1mm / $70k MHI) and many many other major league metro areas.

The wealth and population of the west coast is hard to conceive for outsiders. LA gets its time on screens but if Seattle, Portland or the Bay ever appear in pop culture it’s usually for some natural scenery, suburban sparse setting and noir-ish deserted urban spaces. The raw demographic weight of people and cash in this narrow strip is rarely felt.

Some might say “yeah but it’s a high cost of living (COL) area, so do they really have more disposable income?” Not everyone of course, but some do and the beauty of a high COL area for something like the NBA is that your major cost basis (the cap) is fixed to a national standard but your customers are looking at prices on a local scale. High COL means your competition for local consumer event dollars is charging more for everything but your competitors for talent are paying the same salaries as you. In Seattle you can charge far more for tickets and goods than you can in other rival NBA cities which would be subject to the same salary floor and cap as you. And of course high COL and MHI means your advertising minutes are worth more.

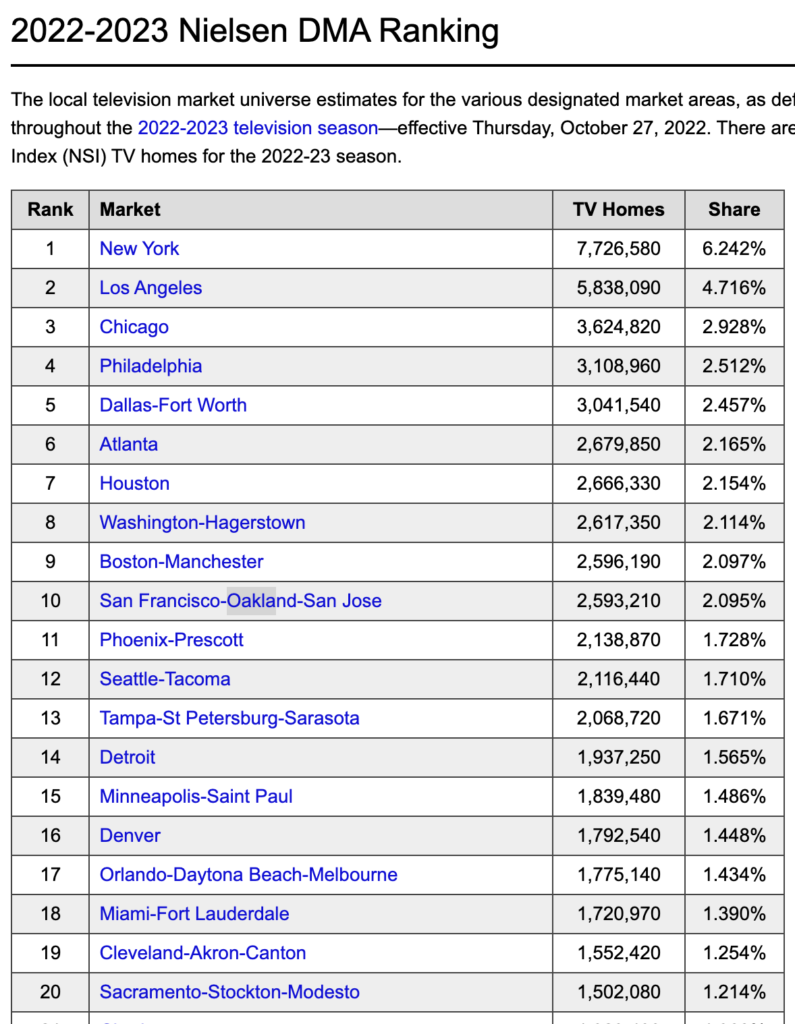

The Nielsen TV homes market rankings is an imperfect tool but here is the 2022 list:

You’ll note that every other market in that top 20 has an NBA team except for Tampa.

This is nothing new: Seattle was 14 in 2008 and 13 in 2009.

If you think I’m being exceptionally cold in making such a big deal about wealth, bear with me we’ll bring it back.

Of course there are non-financial concerns. Our ideal NBA city should also have long dark winters, (Seattle is north of Toronto and Minneapolis), but without too much snow to keep people housebound. No mild weather activity competition like Miami and San Diego. It should have already shown it can be fanatically devoted to a team. And better yet, an NBA team. An NBA team with an NBA championship! All that hard-earned cultural capital, the iconic green and yellow uniforms. The Pearl Jam videos. How could you forego all that?

Correcting the record

This is the company line: “The Sonics were losing money and Howard Schultz tried and tried to get a new arena but the public wouldn’t put up money so they sold in frustration.” The “Sonic Boom” podcast is a very useful resource but the degree to which they swallow this line and don’t check facts made me very frustrated.

They rely heavily on Wally Walker as a friendly source. In their own words: “Perhaps no man has as deep of a history with the Sonics as he does. He won a title there in ’79, became the GM during the Kemp-Payton years of the ’90s, joined Schultz’s ownership group, and became CEO in 2001. For Wally, everything that was about to happen in this story feels personal. This wasn’t just business for him.”

The problem with that is he has a deep personal stake in explaining away why the late 90s teams underperformed and why the ownership group felt they had to sell. Let’s work backwards from the end. Here in The Ringer’s partial transcript of the podcast is the most suspicious passage:

But still, it looked like they might sell. At this point, in 2006, it was hard to tell how much NBA franchises were worth. The TV boom hadn’t quite yet hit the league.

Teams were still heavily dependent on revenue generated from ticket sales. But the ownership group was trying to figure out a price tag that made sense.

“I just threw it out there cause I thought the $350 million—sounds crazy now with the franchise values—no one would pay,” Walker says.

Sonic Boom episode 5

The TV revenue lie

I don’t mean to be too hard on Sonic Boom because they did a yeoman’s job in tracking and recreating the story but this short passage contains two massive checkable falsehoods. Let’s start with this sentence that they themselves originate “The TV boom hadn’t quite hit the league.” As we covered in parts 1 and 2 the TV boom was well underway by the mid-1980s and had most assuredly hit the league in 2005. In fact, the Schultz ownership group were beneficiaries of one of the boom’s many delightful upward shocks.

News of TV rights megadeals with ESPN are archived on ESPN itself

NBA TV deal moves to ABC, ESPN

Tuesday, January 22, 2002ABC, ESPN, TNT and a new national cable sports network jointly owned by the NBA and AOL Time Warner all will show NBA games starting with the 2002-03 season. The total deal is worth a reported $4.6 billion, and leaves NBC without the NBA for the first time in 12 years.

The deals are worth $765 million a year, a 25 percent increase from the $615 million the league made annually in TV rights under the four-year, $2.46 billion deals with NBC and Turner Sports that expire after this season.

NBA teams received $23 million per season from the current NBC deal. If the estimates on Turner’s portion of the deal are close to correct, teams would receive $27 million per season, starting next year.

https://www.espn.com/nba/news/2002/0122/1315389.html

But nationwide is not the only TV money. Teams can have their own local cable deals which are as lucrative as the local market will bear.

FSN Northwest Feeling SuperSonic

MultiChannel News article by Mike Reynolds, January 23, 2004 archived here.

Fox Sports Net Northwest reached a multiyear agreement Friday with the Seattle SuperSonics to air up to 70 of the National Basketball Association club’s games beginning next season.

With the deal, terms of which were not disclosed, FSN supplants local stations KING-TV and KONG-TV as the team’s carriers. Combined, the stations are airing 56 Sonics games in the 2003-04 season.

A FSN spokeswoman said the regional sports network has the right to produce and air a minimum of 70 games each season over the course of the deal, while retaining the right to offer some on broadcast. “Our intention is to present them all,” she added.

And yes that does appear to be an Oasis reference in that headline from MultiChannel News:

So during the short Schultz tenure there were two major TV deals signed. How much was that FSN Northwest deal worth? Unfortunately I cannot find a number in any research. Here’s an interesting article from the New York Times vault: The Cable Guys, May 14, 2002. It’s all about how incredibly well the Mariners games do on cable thanks to faithful Seattle sports fans.

Fox Sport Northwest is paying dearly to carry the Mariners. A new deal that began last season paid the team $37 million, one of the steepest payments in baseball. The previous year, the fee was $18 million. The cable channel carries 107 games.

NYT 5/14/2002 details above

107 Mariners games were worth $37mm… at a straight conversion on game count that would put the Sonics deal in the ballpark of $24mm. The Mariners were probably more popular at that point, but winter TV inventory is more valuable, so I think the ballpark of $20mm+ is reasonable.

There is of course another independent revenue and value estimator out there: Forbes magazine’s yearly franchise value estimates. I don’t like relying on them because they have a history of letting owners steamroll them with whatever lowball narrative the owners are pushing but it’s a useful piece of info for triangulation.

- 2004 Forbes Sonics report (archived)

- 2005 Forbes list (with revenue estimates)

- 2006 Forbes Sonics report

(Here’s a great example of Forbes thinking: In 2005 they valued the Sonics at $234mm. In 2006 the team sold for $350mm and immediately after they valued the team at… $268mm. Here at Forbes we respect capital markets and when seasoned billionaire businessmen put hundreds of millions of dollars on the line at a given valuation we calmly say “no that’s wrong.”)

The Forbes blurb for 2006 also repeats the ownership group line about “heavy losses” but the only year that shows losses is 2005. Anyway here are their revenue estimates for the Sonics:

| Year | Total Revenue | Gate | Salary Cap |

|---|---|---|---|

| 2004 | 70 | 23 | 43.8 |

| 2005 | 81 | ?? | 49.5 |

| 2006 | 81 | 24 | 53.1 |

Using Forbes as our guide we can get a rough sense that our estimate of $20mm in local TV revenues is in the ballpark: The delta between gate and total is over $50mm and $27mm of that is from the national deal.

(Those 2005 losses? I would bet it was dominated by new stadium PR & lobbying. “Sonic Boom” contains the detail that Paul Allen spent $11mm in the election year to push through the football stadium referendum.)

Key points: TV was huge by 2006, it’s absurd to say “the boom hadn’t reached the league.” I’ve included the cap number so you can see how sweet the numbers are: A team like the Sonics can run a full-cap payroll and break even on player salaries just from the non-gate “passive” revenue alone. A more accurate rephrasing of the first sentence would be: “With the TV boom in full effect, NBA owners had come to see in-person revenues as 100% gravy and made every effort to coerce the public to pay for the facilities that maximized them.”

The valuation lie

If you set a price for your asset and someone calls up and offers you your number within a pretty short time, there are two possibilities:

- You are anxious to sell and the number you set was on the low side of fair.

- You wildly and incompetently misread the market.

This is a tautology! One or the other must be true. It’s amazing that journalists in a business piece would let the subject get away with this hand-waving “The counterparty is cuh-razy for meeting my price” narrative. Let’s take a look at recent NBA franchise sales when Walker set that price:

| Date | Team | Sale Price |

|---|---|---|

| Jan 2000 | Dallas | $285 |

| Jan 2001 | Seattle | $200 |

| Dec 2002 | Boston | $365 |

| Jan 2004 | Nets | $300 |

| April 2004 | Charlotte | $300 |

| July 2004 | Phoenix | $401 |

| Jan 2005 | Cleveland | $375 |

Without the benefit of hindsight at the subsequent price run-ups, using only the market climate in late 2005, we can see that $350mm for the Sonics is an entirely reasonable valuation given the contemporaneous NBA franchise dealflow.

(I’m excluding the 2004 Atlanta Hawks deal here because it was a package deal with a very distressed NHL asset on the eve of the NHL lockout. And also because I believe it to be a bald act of insider collusion to asset-strip Time Warner during a particularly contentious period. Seriously.)

Let’s take a look at another simple metric: revenue multiples. This is going to sound simplistic, but businesses are valued based on how much revenue they can generate. Obviously there are plenty of caveats and multiples are different depending on industry, company maturity and everything else but in general, adding revenue to your top line is going to move the business value much more than finding savings in your bottom line. Most people understand this instinctively but business journalists seem to forget it when it comes to specific examples.

If a sleepy corner store is valued at 3X revenue and it cuts costs to achieve 10% greater profits that’s not going to move the valuation the way unlocking 10% greater revenue would. A growing software company might be valued at 15X revenue. If it grows revenue it can keep that multiple but if it simply cuts costs the valuation likely won’t change.

Private Equity vs Venture Capital vs Howard Schultz

Let me offer a gross generalization about investing in private companies: Your style is either VC-coded or PE-coded. VCs want to take growing companies showing good revenues and make them vastly bigger by applying razzle-dazzle magic to make the number go up. The end game is a higher valuation. They don’t care about profits because all the numbers are going to get so much bigger that it’s not worth getting bogged down on today’s losses. PEs, on the other hand, look at existing revenue streams and see juicy overhang that they can hollow out from within and take profits after the reorg. They don’t care about existing profits because they feast on troubled companies with revenue but no profits. Revenue is everything for everyone for different reasons.

(What about sane companies with decent profits and revenue growth? Well as the old commercials used to say: “There’s a list of them printed everyday.” That’s what the public markets are for.)

The problem with being a VC is you’ve got to make the number go up, otherwise you just upset everyone and burn cash on nothing. You’ve got to be a salesman and huckster and inspire a growing workforce and actually build out product. The problem with being a PE is you’ve got to have technical mastery of the field and iron discipline and a stomach for being hated. In our modern West Coast era the Lacob Warriors are a VC-style team. The Fisher Oakland As are the ultimate PE team. Lacob’s high-spend new-everything press-your-luck mix has worked to grow valuation to untold heights but Fisher has probably banked more cash over the last 10 years. ($62mm in revenue sharing last year alone according to reports!) He’s steadfastly refused to sign longterm contracts, juiced the stadium without investing, strung the city along and now when he’s hated beyond measure he’s about to leave town for another sucker. (Sports teams can’t actually go public but the SF Giants seem to me a public-coded team: they keep their ownership group happy and in line but the product gets some investment too.)

My take on Schultz is that he thought he could be a VC. He was a number-go-up magic man with Starbucks. How hard could it be? But it just didn’t work out and he lost his nerve. His shtick wasn’t working and the grind got him down. The personal touches rubbed everyone the wrong way. (Gary Payton has some amusing rants on the podcast about his personal animus toward Schultz.) His career has a few of these tone deaf moments: the absurd Starbucks “Race Together” campaign that he thought would spark a national moment of racial harmony but instead just got laughed at. His presidential campaigns that inspired exactly no one. Wikipedia: “Schultz publicly considered a candidacy in the 2012, 2016, and 2020 U.S. presidential elections as an independent candidate. He declined to join all three contests.”

Stalling out in the arena bid was more than just a monetary setback, it was a failure of an entire mien and of his belief in himself as something special. From Wikipedia quoting his autobiography: “Selling the Sonics as I did is one of the biggest regrets of my professional life. I should have been willing to lose money until a local buyer emerged. I am forever sorry.” That teary mea culpa is cover. He wasn’t losing money. He sold because he had to face a failure in his approach to life. On the financial side there was ample time for a graceful reset to a “public” style ownership or just reset of goals and timeline cushioned by ample revenues. But not on the personal side.

Priced to sell

NBA teams are businesses with growth potential somewhere between sleepy corner stores and hot software companies. Journalism tends to hand-wave around the details of the growth in sports franchise values and attribute it to “glamor”, or inflation per se, or some over-supply of billionaires. But the main reason is the trend we’ve been hammering since part 1: Sports became much more profitable without becoming more popular. Sports franchises have been growing revenues and they trade for multiples somewhere between 4X and 8X revenue.

Given all that Wally Walker knew about the internals of the business, the revenue number from the two very significant TV deals that had been signed since the Schultz group bought the team, it was entirely reasonable to set a price around 5X revenue. Very, very reasonable. A little too reasonable. There is no chance they made that price point thinking “this is crazy.”

That’s the underlying problem with the Sonic Boom narrative and the insiders it relies on. They’re starting from a foundation of institution-friendly lies that they never challenge.

Even this skeptical narrative that tries to ask pragmatic questions about where self-interest lies in the whole affair fails because it accepts certain ground truths from Stern-aligned ownership interests. The whole familiar rogue’s gallery of Clay Bennett and Howard Schultz and Frank Chopp is beside the point: this never should have happened.

What was really going on with the rest of the ownership group?

Do you remember the period 2003-2007? The stock and real estate markets were on an absolute tear. It was the bubble forming before the 2008 crash. $100 in the S&P in 2003 would have turned into $170 by the end of 2006. (A 14% annualized return.) For Schultz and his group of 57 minority investors it’s easy to convince yourself you’re losing money when you’re marking an illiquid investment with single-digit margins against the froth in the public markets.

Closer look at the Frank Chopp details

“Sonic Boom” has a nice little section about Stern’s encounter with Washington State House Speaker Frank Chopp. In short: Stern flew all the way out to Olympia to lobby for public money and Washington’s own Lyndon Johnson-esque power broker shut him down. Chopp didn’t give Stern much of a chance and he made him feel like he wasted his time. We don’t know exactly how this contributed to the final outcome but it certainly feels like Stern to take this slight and spit it back seven-fold at the people of Washington.

Cui bono?

So the Seattle move was bad for the financial future of the league, founded on lies, generation-defining terrible for the Seattle fans… who was it good for?

NBA franchise owners. That’s it. By sacrificing Seattle, Stern showed he was willing to let any city fall that dared withhold public funds. At the same time he created a potent perpetual vacancy to further scare existing cities. Much like the NFL with its post-1995 hole in Los Angeles, keeping a class-A city without a team hurts fanship and general revenue while pumping up the goodies that cities feel forced to dole out directly to other owners.

What about OKC fans don’t they deserve a team?

I guess, sure. Not relevant. “Do no evil so that good may come.”

Conclusion

Why is it so much about money? That’s what we’re always being told is the special core of Stern’s actions for good. The revenues! The increasing number of fans! But here we see his [in]direct action to sever the NBA from a huge revenue market and a huge group of fans.

It was financial malpractice to let a team leave the lucrative Seattle market. The Sonics were in a perfectly fine place financially and the buyout offer the ownership group took was reasonable but not excessive. What Stern “let happen” was in direct contravention of his “business genius” but it just so happens was very good for creating leverage for his owners to extort new public spending for stadiums. In the end if you “let” something this bad happen you have in fact made something happen.

A scandal like this should have destroyed Stern’s reputation as a mastermind and the image of his reign being in any way good for fans. But instead we all just moved on and he ruled for another seven years.